Interchangeable Lens Shipments in 2025: What the Latest CIPA Data Shows

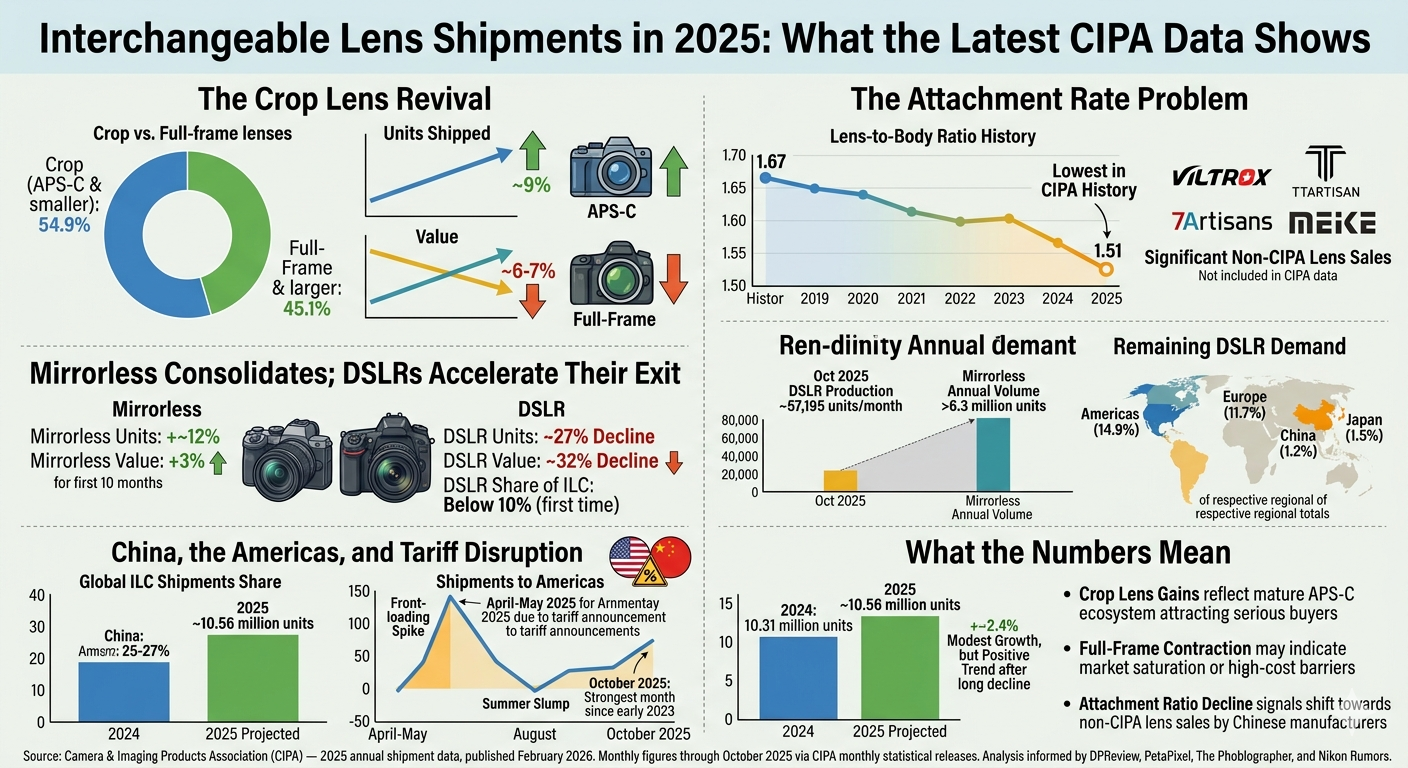

The Camera & Imaging Products Association published its full 2025 shipment figures in February 2026, completing the picture of a year defined by two diverging trends: crop-sensor lenses gaining ground in units while full-frame glass quietly contracted, and an industry-wide lens-to-body ratio that hit the lowest point in CIPA’s recorded history.

The Crop Lens Revival

The most consequential shift in the 2025 data is the performance gap between sensor formats. Lenses for APS-C and smaller sensors rose approximately 9 percent in units and 21 percent in value through the final reporting period, while lenses for full-frame and larger formats declined around 4 to 5 percent in units and 6 to 7 percent in value. By the end of the year, crop lenses made up 54.9 percent of total interchangeable lens shipments, with full-frame accounting for the remaining 45.1 percent — a narrower margin than in previous years, but still a crop-majority result.

This is not the story the industry’s marketing cycle tells. The camera press of 2025 was dominated by full-frame launches, pro-grade mirrorless bodies, and premium optics announcements. The actual shipment data points in a different direction: more people were buying into APS-C systems, and they were paying more for crop lenses than in prior years — a sign that the segment is maturing beyond kit zoom territory.

The Attachment Rate Problem

The more structurally significant number in the 2025 dataset is the lens-to-body ratio. Historically, CIPA’s data showed approximately 1.67 lenses shipped for every interchangeable lens camera — a figure stable enough that only events of global scale could move it. In 2025, that ratio fell to 1.51, the lowest in the association’s history, continuing a decline that has now extended across multiple consecutive years.

The most credible explanation is not that photographers are buying fewer lenses, but that a growing share of lens sales is occurring outside CIPA’s reporting universe. Chinese manufacturers — Viltrox, TTArtisan, 7Artisans, Meike, and others — are not CIPA members, and their output is entirely absent from these figures. As those brands have matured and expanded into full autofocus lens lines compatible with Sony E, Fujifilm X, and Canon RF mounts, they have begun capturing a segment of the market that CIPA simply cannot see. The association’s own published member list, last updated in March 2026, confirms the exclusion.

Mirrorless Consolidates; DSLRs Accelerate Their Exit

Through the ten months of 2025 for which detailed breakdowns are available, mirrorless shipments were up approximately 12 percent in units but only 3 percent in value — indicating a shift toward mid-range bodies rather than the high-ASP flagships that drove value growth in earlier years. The DSLR segment fell roughly 27 percent in units and 32 percent in value over the same period, with the DSLR share of interchangeable lens camera shipments dropping below 10 percent for the first time. October 2025 production ran at approximately 57,195 DSLR units per month, against cumulative full-year mirrorless volumes on pace to close above 6.3 million units.

The geographic skew of remaining DSLR demand is notable. The Americas and Europe absorbed the bulk of what was still shipping — accounting for 14.9 and 11.7 percent of their respective regional camera totals — while China and Japan had essentially moved on, with DSLRs representing just 1.2 and 1.5 percent of those markets.

China, the Americas, and Tariff Disruption

China remained the largest single destination for interchangeable lens cameras in 2025, accounting for roughly 30 percent of global ILC shipments, followed by the Americas at 25 to 27 percent. The American figure, however, carries an asterisk. The Trump administration’s tariff announcements in April 2025 triggered a front-loading spike in shipments through April and May as manufacturers raced to land inventory in the US ahead of implementation. The resulting hangover produced a sharper-than-usual summer slump in August, visible in the monthly data and noted in CIPA’s own tracking. By October, volumes recovered — October 2025 became the strongest single month for camera and lens shipments since early 2023 — but the tariff effect remains a structural variable for 2026 planning.

What the Numbers Mean

The 2025 CIPA lens data is a market in genuine, if uneven, recovery. Total lens shipments for the year were projected to finish around 10.56 million units, up approximately 2.4 percent from 2024’s 10.31 million — modest growth, but growth in a category that had declined every year from 2013 through 2022 with only minor exceptions. The trajectory is positive; the composition is shifting.

The crop lens gains are real and likely to continue. The APS-C mirrorless ecosystem — Fujifilm X, Sony APS-C, Canon R7/R10, Nikon Z50 series — is now mature enough to attract serious buyers, not just entry-level ones, and the expanding catalog from non-CIPA Chinese manufacturers adds further depth that the official numbers cannot capture. The full-frame lens contraction is harder to read in isolation: it may reflect saturation among existing mirrorless adopters who upgraded glass in 2021 to 2023 and see no need to buy again, or it may reflect a ceiling in the addressable market for high-cost optics at current price levels.

The attachment ratio decline is the signal worth watching most closely. If it continues into 2026 — and there is no structural reason to expect a reversal — it will increasingly reflect a camera industry whose official statistics are being quietly rewritten by manufacturers that have chosen not to join the organization tracking them.

Source: Camera & Imaging Products Association (CIPA) — 2025 annual shipment data, published February 2026. Monthly figures through October 2025 via CIPA monthly statistical releases.